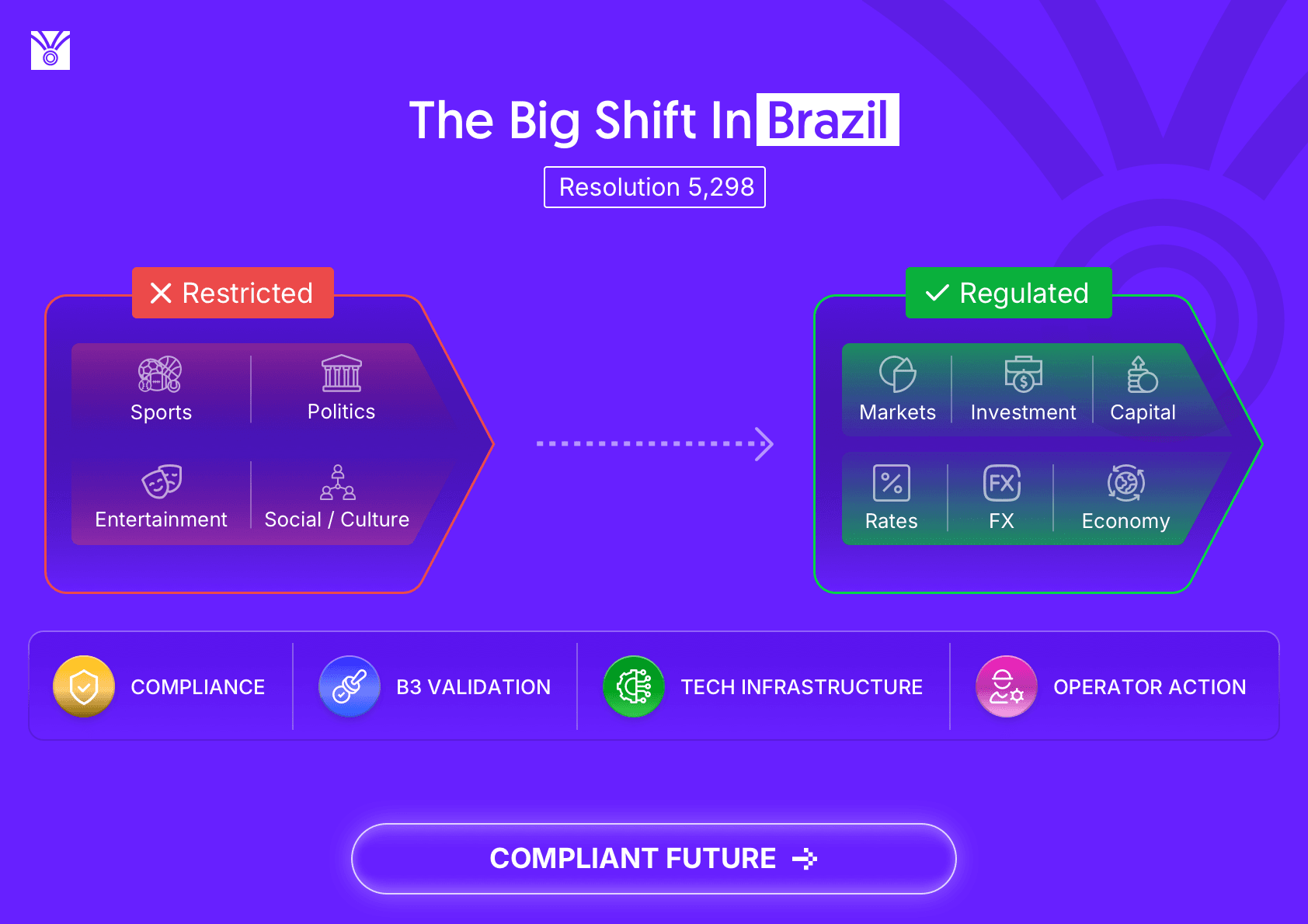

Brazil’s prediction market landscape changed almost overnight. For months, prediction markets — letting users trade views on politics, sports, entertainment, culture, crypto and macroeconomics — were one of the most exciting categories in digital trading. Then came CMN Resolution No. 5,298, and the message turned sharp: non-financial prediction markets are no longer treated as an open playground.

The Brazilian government has moved against platforms that, in regulators’ view, were operating too close to unregulated betting. Reuters reported that Brazil blocked prediction-market platforms and tightened derivatives rules, with the National Monetary Council defining which underlying assets may be used. The new framework bars derivatives linked to sports, online gaming, political, electoral, cultural and social outcomes — while allowing only contracts tied to economic and financial benchmarks such as price indices, interest rates and exchange rates.

This is not the end of prediction markets in Brazil. It is the beginning of a more serious version of them. The future is not “anything can be traded.” The future is regulated financial event contracts.

For operators, brokers, fintechs, exchanges and licensed financial firms, that creates a single strategic question: how do you move from informal prediction markets to compliant, financial-grade event-contract infrastructure?

The regulatory shift: Brazil is separating bet-like markets from financial derivatives

Resolution No. 5,298 is not simply a ban on innovation. It is a line of separation.

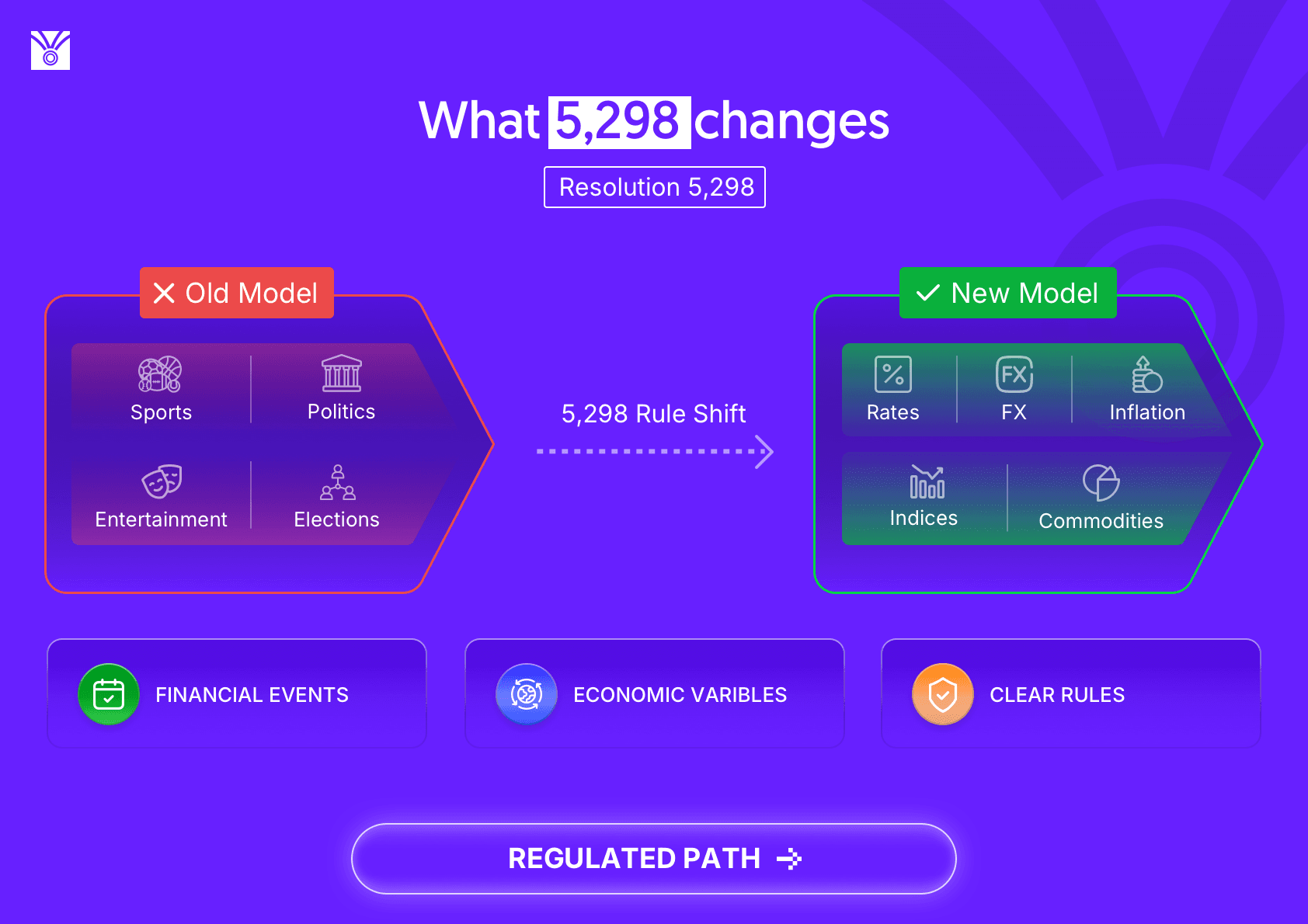

On one side: event markets linked to non-financial outcomes — sports, elections, political themes, reality shows, entertainment. Agência Brasil confirmed these categories are now prohibited under the new rule, even when foreign platforms offer such products to Brazilian users.

On the other side: contracts linked to economic and financial variables — interest rates, inflation, exchange rates, commodities and other financial references — which remain possible under CVM supervision. The text of Resolution No. 5,298 permits derivatives that reference commodities, financial assets, securities traded on authorized infrastructure, and other economically relevant variables based on consistent, verifiable methodologies. It enters into force on 4 May 2026.

For serious operators, the strategic question changes. It is no longer: “Can we launch a prediction market like Polymarket?” It becomes: “Can we build a regulated financial event-contract platform that aligns with Brazil’s securities and derivatives framework?”

One model looks like gaming. The other looks like financial infrastructure.

Why B3’s event contracts validate the model

The timing of Brazil’s regulatory action matters because it is happening alongside another major development: B3’s move into event contracts.

B3 describes its event contracts as products that let investors take positions on future scenarios involving indices, currencies, cryptocurrencies and economic indicators — traded under CVM and BSM supervision, with clear prices, public methodologies, guaranteed settlement, fixed payout and maximum loss known at trade entry.

The signal is unmistakable. Brazil is not rejecting the event-contract concept. Brazil is rejecting unregulated, non-financial, bet-like versions of it.

B3’s own documentation lists potential underlying references such as Spot Bitcoin, Spot Ethereum, Spot Solana, Spot U.S. Dollar, Bovespa Index, Monthly IPCA, GDP, and futures on Bitcoin, Ethereum, Solana, Mini U.S. Dollar and Mini Ibovespa.

The direction is clear. The future of prediction markets in Brazil is financial, regulated, transparent, settled against trusted data, and built on serious infrastructure. A very different category from casual betting — and a much larger, more sustainable opportunity.

The gap: professional investors have B3, the wider market still needs compliant access

B3’s initial event-contract model is not built for the mass retail audience. iGaming Business reported that CVM initially restricted B3 event trading to professional investors with more than R$10 million in assets, with binary “yes/no” scenarios on the dollar, Ibovespa and bitcoin.

That creates a major gap. Brazil has a large, increasingly sophisticated retail trading culture. Investors already understand crypto, FX, indices, short-term volatility and macroeconomic events. But the compliant event-contract model today sits with institutional infrastructure.

This does not mean any company can simply launch a mass-market version tomorrow. Legal structure, licensing, product approval, KYC, suitability, responsible-trading rules, risk controls, settlement methodology and regulator engagement all matter.

But one thing is clear: the demand is not going away. It is moving from the grey zone into regulated financial architecture. Operators who understand this shift early will hold the advantage.

From prediction market to financial event-contract platform

For operators affected by Resolution No. 5,298, the transition is not cosmetic repositioning. It is a complete change in product philosophy.

| Old prediction market ask | Financial event-contract platform ask |

|---|---|

| Will Team A win tonight? | Will USD/BRL close above a defined level? |

| Will Candidate X win the election? | Will Bitcoin settle above a specific reference price? |

| Will this celebrity win the reality show? | Will Ibovespa finish the day above a strike level? |

| Will monthly IPCA come in above market expectation? | |

| Will the Selic rate change at the next meeting? |

That difference reshapes the entire infrastructure stack. A financial event-contract platform needs reliable market-data feeds, transparent contract creation rules, clear reference prices, defined expiry and settlement logic, audit trails, risk controls, KYC and suitability, liquidity architecture, real-time pricing, responsible-participation limits, regulatory reporting readiness, and integration with local payment rails.

This is not a betting product with a financial skin. It is a financial technology platform with event-based engagement.

What Resolution No. 5,298 compliance means for technology teams

For CEOs and CTOs, “Resolution No. 5,298 compliance” should not be treated as a single legal checkbox. It should become a product-architecture principle.

Every market must trace back to a permitted economic or financial reference. Every data source must be verifiable. Contract rules must be clear before the user enters the trade. Payouts must be deterministic. Settlement must be auditable. The operator should be able to show why a contract exists, what it references, how it was priced, how it was traded, and how it was resolved.

Older prediction-market platforms will struggle here. They were designed for breadth — any question, any topic, any outcome. Brazil’s new environment rewards depth — fewer categories, stronger rules, better infrastructure, trusted settlement. That is why serious operators need a CVM event-contracts tech provider, not just a white label prediction market vendor.

The architecture serious operators will need

A compliant financial event-contract platform should be built around five core layers.

1. Market creation engine

Operators need to spin up markets around approved financial references — currencies, indices, crypto, inflation, interest rates, commodities, other economic indicators — manually, via templates, or with AI-assisted generation. Every market must have a clear reference source, defined expiry, fixed settlement rule and pre-approved category. AI can suggest high-quality market ideas; the compliance framework decides what actually goes live.

2. Real-time data and oracle layer

In financial event contracts, trust depends on data. Integrate with reliable feeds — exchange data, official government statistics, central bank publications, approved market-data providers. Resolution sources must be visible and auditable. Users should not feel the platform “decided” the outcome; they should see it was settled against a defined source. This matters most in short-duration contracts, where small delays or ambiguous timestamps create disputes.

3. Exchange-grade trading engine

Once event contracts become financial products, the backend cannot behave like a casual gaming system. It needs real-time order handling, price updates, exposure controls, wallet reservation, settlement queues, concurrency handling and WebSocket-driven market updates. Depending on the model, the platform may run a Central Limit Order Book, an Automated Market Maker, a hybrid CLOB+AMM, or fixed-payout binary logic. (B3’s event contracts use fixed payout — BRL 100 with tick size 0.01 points, similar in structure to COPOM Options.)

4. AI-assisted market generation and resolution

Financial markets move fast; pure manual market creation misses the moments that drive user attention. AI can scan financial events and feeds, suggest market questions, and assist in resolution against verified sources — but admin review, rule and duplication checks, audit trails and override authority must remain. AI suggests; the compliance framework decides; humans retain control. This is what gives operators speed without losing discipline.

5. Compliance, KYC, suitability and responsible-trading controls

If regulators are concerned about gambling-like behaviour, financial event-contract platforms must be built with guardrails from day one: KYC and liveness verification, suitability checks, risk warnings, position and loss limits, cooling-off rules, self-exclusion, deposit limits, market-category restrictions, audit logs, admin approval workflows, suspicious-activity monitoring, geo controls and reporting dashboards. The user experience can stay simple. The infrastructure behind it cannot.

Liquidity and short-term contracts: where design discipline shows

Two questions sit at the centre of every financial event-contract business: how to provide liquidity, and how to handle short-duration products safely.

Liquidity models

Three models are possible. A pure order book, where buyers and sellers post orders and price emerges from trading. An Automated Market Maker (AMM), where the platform provides algorithmic liquidity along a pricing curve. Or a hybrid, where an order book is supported by AMM or external liquidity partners. For a new market, hybrid is usually the most practical starting point — users get a better experience before organic depth builds. Either way, the admin must control maximum exposure, market-specific limits, spreads, liquidity budgets, suspension rules and abnormal-movement alerts. Liquidity without exposure controls quickly becomes platform risk.

Short-term contracts

Modern traders are comfortable with fast decisions and bounded risk, which makes 5-minute, 15-minute, hourly and event-window contracts powerful — for example, Will Bitcoin be above this level in 15 minutes? Will USD/BRL move above this level by the next fixing window? But the shorter the duration, the more the platform must care about data latency, manipulation resistance, exposure limits, feed reliability and settlement precision. Short-duration financial event contracts demand exchange-style infrastructure, timestamp discipline, automated resolution, pre-trade rule clarity and compliance gates. Treat them as financial products, not gaming features.

A phased roadmap for operators

If you are an operator, broker, fintech, or financial firm evaluating legal prediction market alternatives in Brazil, the immediate roadmap should focus on implementing scalable prediction market software solutions in a practical and compliant way.

First, separate non-financial markets from financial event contracts. Sports, politics, entertainment and social-event markets now carry a very different regulatory risk profile. Second, identify the financial references that may suit your business — USD/BRL, Bitcoin, Ibovespa, Selic, IPCA, commodities or other economic indicators. Third, work with Brazilian legal counsel on licensing, product structure, target user category, suitability requirements and approval pathway. Fourth, design the technology around compliance from line one. Do not build a flexible “anything market” engine and try to restrict it later.

A sensible phased launch:

- Phase 1 — Admin-controlled financial event contracts on a narrow set of references.

- Phase 2 — Market data-feed integration and automated resolution.

- Phase 3 — CLOB or AMM liquidity layer.

- Phase 4 — AI-assisted market generation.

- Phase 5 — Advanced risk controls, reporting and scaled user access.

- Phase 6 — Potential retail expansion, subject to legal and regulatory approvals.

This lets operators move forward without rushing into avoidable risk.

The commercial opportunity: serious users, higher trust, longer lifetime value

The old prediction-market model often attracted casual attention. Financial event contracts attract a different kind of user — one who already trades crypto, FX, equities or derivatives, follows markets, understands risk, values transparent settlement and wants speed with bounded exposure. That user typically carries far higher lifetime value than a casual bettor.

A well-built financial event-contract platform can become a trading-engagement layer for brokers, a new product vertical for fintechs, a retention engine for crypto platforms, a macro-event trading product for sophisticated users, and a compliant alternative for operators moving away from prohibited categories.

In the old model, prediction markets were a novelty. In the new model, event contracts become part of the financial trading stack — a much bigger opportunity.

Why the timing matters now

The market is at an unusual moment. Resolution No. 5,298 takes effect on 4 May 2026. Brazilian authorities have already moved against existing platforms — Reuters reported that sites such as Polymarket and Kalshi were taken offline in Brazil after action by Anatel. At the same time, B3 is actively validating regulated event contracts as a financial-product category, with documented emphasis on regulated trading, transparency, guaranteed settlement, fixed payout and limited risk across indices, currencies, crypto and economic indicators.

The unregulated version is under pressure. The regulated version is being validated. Operators who act now will define the next category.

Conclusion: event contracts as financial infrastructure

Brazil’s Resolution No. 5,298 is a turning point. It closes the door on a broad, unregulated, non-financial prediction-market model. It opens the door to something more durable: financial event contracts built on regulated infrastructure, trusted data, transparent settlement and serious risk controls.

For operators, this is not the time to rebrand. It is the time to rebuild.

The companies that win will be the ones that understand the new reality: prediction-market excitement must now meet financial-market discipline.

Vinfotech is built to support that. As a technology partner for financial prediction markets and event-contract platforms, we help licensed operators, fintechs, brokers and market innovators build the infrastructure this category demands — CLOB and AMM trading engines, real-time WebSocket infrastructure, AI-assisted market creation and resolution, market-data feed integrations, admin risk controls, KYC and wallet workflows, audit logs and reporting dashboards, and compliance-ready architecture for licensed operators.

If you are evaluating Resolution No. 5,298 compliance, looking for a CVM event-contracts tech provider, or exploring legal prediction-market alternatives in Brazil, the next step is not to copy the past. It is to build the regulated future.

Let’s build Brazil’s next generation of financial event-contract platforms.

Frequently Asked Questions

What is Resolution No. 5,298 in Brazil?

Resolution No. 5,298 is a CMN (National Monetary Council) rule that changes how derivatives linked to future events may operate in Brazil. It restricts non-financial event contracts (sports, political, electoral, cultural, social outcomes) and allows derivatives tied to defined economic and financial references, subject to applicable regulation and CVM supervision.

When does Resolution No. 5,298 take effect?

Resolution No. 5,298 enters into force on 4 May 2026. Operators with exposure to Brazilian users — including foreign platforms — should treat this date as the deadline for aligning product structure, market categories and compliance architecture.

Are prediction markets banned in Brazil?

Non-financial prediction markets linked to sports, politics, elections, entertainment, cultural and social events are now heavily restricted. However, financial event contracts linked to economic variables — inflation, interest rates, exchange rates, commodities and other financial references — may still be possible under the appropriate regulatory framework.

What types of event contracts are still allowed?

Contracts referencing economic and financial variables remain permitted. Examples include FX (USD/BRL), interest rates (Selic), inflation (IPCA), equity indices (Ibovespa), commodities and crypto assets such as Bitcoin or Ethereum — provided the contract uses a verifiable methodology and runs under CVM supervision.

What are B3 event contracts?

B3 event contracts are regulated financial products that allow investors to take positions on future scenarios involving indices, currencies, cryptocurrencies and economic indicators. B3 describes them as transparent, limited-risk products with public methodologies, fixed payout (BRL 100 per contract) and guaranteed settlement under CVM and BSM supervision.

Can retail users trade financial event contracts in Brazil?

B3’s initial model has been reported as restricted to professional investors with more than R$10 million in assets. A broader retail-facing model would require careful legal structuring, licensing, product approval, suitability checks, responsible-trading controls and regulatory alignment.

What is the difference between a prediction market and a financial event contract?

A prediction market typically asks any-topic, outcome-based questions across politics, sports or entertainment. A financial event contract is a regulated derivative tied to a verifiable economic or financial reference, with defined expiry, deterministic payout and auditable settlement. The first looks like gaming the second is financial infrastructure.

What technology does a financial event-contract platform need?

At minimum: a market-creation engine tied to approved references, a real-time data and oracle layer, an exchange-grade trading engine (CLOB, AMM, hybrid or fixed-payout binary), AI-assisted generation and resolution with admin review, and a full compliance stack — KYC, suitability, position limits, cooling-off, audit logs and reporting.

What should operators do after Resolution No. 5,298?

Stop treating prediction markets as a broad entertainment category. Identify permitted economic references, work with Brazilian legal counsel on licensing and product structure, and design technology around compliance from day one rather than bolting it on later. A phased launch — admin-controlled markets first, automation and retail access later — is usually the safest path.

Can Vinfotech build a financial prediction market platform for Brazil?

Yes. Vinfotech builds custom and white-label financial prediction-market and event-contract infrastructure — including CLOB, AMM, AI-assisted market creation, automated resolution workflows, market-data feed integrations, admin and risk controls, wallet systems, KYC integrations and scalable real-time trading architecture for licensed operators.